Federal Budget review 2020-21

The Treasurer, Josh Frydenberg, delivered the Federal Budget on 6 October 2020. Originally postponed from May 2020 due to the coronavirus pandemic, this Budget has been highly anticipated and here we have a review of its inclusions.

FOR YOU

Personal income tax cuts

Date of effect: 1 July 2020

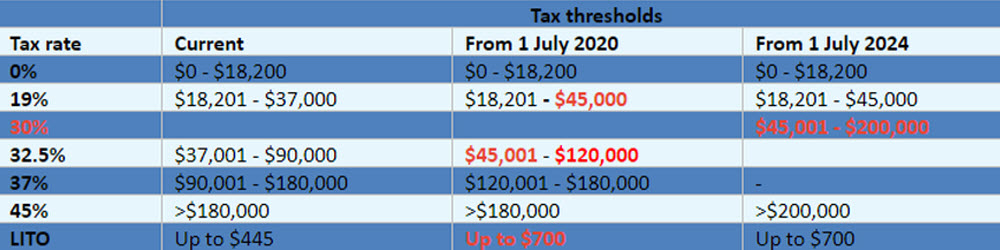

As widely predicted, the Government has brought forward stage 2 of its planned income tax cuts by two years.

Originally intended to apply from 1 July 2022, the tax cuts will come into effect from 1 July 2020 (subject to the passage of the legislation).

At a cost of $17.8 billion over the forward estimates, bringing forward the tax cuts is a controversial move. The Government argues that the measure will “boost GDP by around $3.5 billion in 2020-21 and $9 billion in 2021-22 and will create an additional 50,000 jobs by the end of 2021-22.”

Others in Parliament believe the measure rewards higher income earners and the money could be better spent elsewhere.

The Senate will decide whether the Government’s plan comes to fruition.

Stage 3 of the Personal Income Tax Plan that simplifies and flattens the personal income system remains scheduled for 2024-25.

Bringing forward the personal income tax plan will:

- Increase the top threshold of the 19% tax bracket to $45,000 (from $37,000)

- Increase the top threshold of the 32.5% tax bracket to $120,000 (from $90,000)

- Increase the low income tax offset from $445 to $700

In addition, the LMITO (low and middle income tax offset), which provides a reduction in tax of up to $1,080 for individuals with a taxable income of up to $126,000, will be retained for 2020-21. This measure was to be removed at the commencement of stage 2 of the reforms from 2022-23.

“The Government has brought forward stage 2 of its planned personal income tax cuts by two years — letting taxpayers get tax relief starting from 1 July 2020.”

$250 economic support payments

Date of effect: November 2020 and early 2021

Two additional economic support payments of $250 each will be made to eligible recipients of the following payments and health care card holders:

- Age Pension

- Disability Support Pension

- Carer Payment

- Family Tax Benefit, including Double Orphan Pension (not in receipt of a primary income support payment)

- Carer Allowance (not in receipt of a primary income support payment)

- Pensioner Concession Card (PCC) holders (not in receipt of a primary income support payment)Commonwealth Seniors Health Card holders

- Eligible Veterans’ Affairs payment recipients and concession card holders.

The payments are exempt from taxation and will not count as income support for the purposes of any income support payment.

Capital gains tax removed from ‘granny flats’

Date of effect: 1 July 2021 subject to the passage of the legislation

At present, if you enter into a formal granny flat arrangement with a relative, such as an elderly parent, there is a risk of capital gains tax (CGT) applying.

Announced pre Budget, this measure provides a targeted CGT exemption for granny flats under certain conditions. Under the arrangement, CGT will not apply to the creation, variation or termination of a formal written granny flat arrangement providing accommodation for older Australians or people with disabilities.

The exemption only applies to family arrangements or other personal ties and will not apply to commercial rental arrangements.

10,000 additional places in First Home Loan Deposit Scheme

Date of effect: 6 October 2020

Announced pre Budget, from 6 October 2020 until 30 June 2021, an additional 10,000 places will be available for first home buyers under the First Home Loan Deposit Scheme to support the purchase of a new home or a newly built home. The scheme enables first home buyers to purchase a home with a deposit of as little as 5% without mortgage insurance. There are currently 27 participating lenders across Australia offering places under the First Home Loan Deposit Scheme.

Aged care support

$1.6bn to help elderly stay at home

As previously announced, the Government has committed to a broad package of aged care funding predominantly focussed on helping older Australians remain at home. $1.6 billion has been provided over four years from 2020-21 to release an additional 23,000 home care packages across all package levels.

The number of home care packages will have increased threefold from around 60,300 in 2013 to around 185,500 in 2021.

Aged care industry monitoring and support

An additional $400 million will see an injection in cash for infrastructure supporting the aged care industry including a new serious incident response scheme and monitoring services.

YOUR SUPERANNUATION

Superannuation accounts ‘stapled’ to an individual

This reform will ensure individuals continue to use their existing superannuation fund when they change jobs. The fund will be “stapled” to the individual to prevent the duplication of superannuation fund accounts when changing employers.

From 1 July 2021:

- If an employee does not nominate an account at the time they start a new job, employers will pay their superannuation contributions to their existing fund.

- Employers will obtain information about the employee’s existing superannuation fund from the ATO.

- The employer will do this by logging onto ATO online services and entering the employee’s details. Once an account has been selected, the employer will pay superannuation contributions into the employee’s account.

- If an employee does not have an existing superannuation account and does not make a decision regarding a fund, the employer will pay the employee’s superannuation into their nominated default superannuation fund.

The Government expects that future enhancements will enable payroll software developers to build systems to simplify the process of selecting a superannuation product for both employees and employers through automated provision of information to employers.

Accountability of underperforming funds

Date of effect: From July 2021 (MySuper products) or From 1 July 2022 (non MySuper products)

From July 2021, the Australian Prudential Regulation Authority will conduct benchmarking tests on the net investment performance of MySuper products, with products that have underperformed over two consecutive annual tests prohibited from receiving new members until a further annual test shows they are no longer underperforming.

If a fund is deemed to be underperforming in the first of these annual tests, it will need to inform its members of its underperformance by 1 October 2021. When funds inform their members about their underperformance they will also be required to provide them with information about the YourSuper comparison tool (see below).

Underperforming funds will be listed as underperforming on the YourSuper comparison tool until their performance improves.

Non-MySuper accumulation products where the decisions of the trustee determine member outcomes will be added from 1 July 2022.

Performance transparency

Date of effect: From July 2021 (MySuper products)

A new interactive tool (YourSuper) will enable a comparison of simple super (MySuper) products ranked by fees and investment returns. The tool will also provide links to other MySuper products and show current super accounts if the individual has more than one.

The tool will be administered by the ATO.

Trustee accountability

Date of effect: By 1 July 2021

The obligations on superannuation trustees will be strengthened to ensure their actions are consistent with members’ retirement savings being maximised. By 1 July 2021:

Superannuation trustees will be required to comply with a new duty to act in the best financial interests of members.

Trustees must demonstrate that there was a reasonable basis to support their actions being consistent with members’ best financial interests.

Trustees will provide members with key information regarding how they manage and spend their money in advance of Annual Members’ Meetings.

BUSINESS AND EMPLOYERS

JobMaker Hiring Credit

Date of effect: From 7 October 2020 for 12 months

Eligible employers will receive:

- $200 per week if they hire an eligible employee aged 16 to 29 years or

- $100 per week if they hire an eligible employee aged 30 to 35 years.

The JobMaker Hiring Credit will be paid quarterly in arrears. It will be available for up to 12 months from the date of employment of the eligible employee with a maximum amount of $10,400 per additional new position created.

Employers will need to demonstrate that the new employee will increase overall employee headcount and payroll.

To be eligible, the employee will need to have worked for a minimum of 20 hours per week, averaged over a quarter, and received the JobSeeker Payment, Youth Allowance (other) or Parenting Payment for at least one month out of the three months prior to when they are hired.

Immediate deductions for investment in capital assets

Date of effect: Acquisition of eligible capital assets from 7:30pm AEDT on 6 October 2020 and first used or installed by 30 June 2022

The Government is really keen for business to invest. This measure enables businesses with an aggregated turnover of less than $5 billion to fully expense the cost of new depreciable assets and the cost of improvements to existing eligible assets in the first year of use.

This means that an asset’s cost will be fully deductible upfront rather than being claimed over the asset’s life. While many businesses were already eligible for an instant asset write-off for asset purchases of up to $150,000, this measure does not cap the asset’s cost, and eligibility for the higher instant asset write-off has been significantly broadened and extended (the existing $150,000 instant asset write-off applies to businesses with turnover less than $500 million and will not apply to purchases after 31 December 2020).

Second-hand assets

For businesses with an aggregated turnover under $50 million, full expensing also applies to second-hand assets.

Businesses with aggregated annual turnover between $50 million and $500 million can still deduct the full cost of eligible second-hand assets costing less than $150,000 that are purchased by 31 December 2020 under the existing enhanced instant asset write-off. Businesses that hold assets eligible for the enhanced $150,000 instant asset write-off will have an extra six months, until 30 June 2021, to first use or install those assets.

Small business pooling

Small business entities (with aggregated annual turnover of less than $10 million) using the simplified depreciation rules can deduct the balance of their simplified depreciation pool at the end of the income year while full expensing applies. The provisions which prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out will continue to be suspended.

Ability for companies to carry-back losses

Date of effect: Losses from the 2019-20, 2020-21 or 2021-22 income years

Companies with an aggregated turnover of less than $5 billion will be able to carry back losses from the 2019-20, 2020-21 and 2021-22 income years to offset previously taxed profits in the 2018-19, 2019-20 and 2020-21 income years.

Under this measure tax losses can be applied against taxed profits in a previous year, generating a refundable tax offset in the year in which the loss is made. The amount carried back can be no more than the earlier taxed profits, limiting the refund by the company’s tax liabilities in the profit years. Further, the carry back cannot generate a franking account deficit meaning that the refund is further limited by the company’s franking account balance.

The tax refund will be available on election by eligible businesses when they lodge their 2020-21 and 2021-22 tax returns.

Currently, companies are required to carry losses forward to offset profits in future years. Under the proposed amendments, companies that do not elect to carry back losses can still carry losses forward as normal.

This measure will interact with the Government’s announcement to allow full expensing of investments in capital assets. The new investment will generate significant tax losses in some cases which can then be carried back to generate cash refunds for eligible companies.

Note that loss carry-back rules were introduced some years ago by the Gillard government. The rules were repealed and were only operational in the 2012-13 year.

R&D tax concessions injection and simplification

Date of effect: 1 July 2021

The Government has enhanced its proposed shake-up of the R&D system injecting an additional $2 billion through the Research and Development (R&D) Tax Incentive.

Currently, the R&D Tax Incentive provides the following in respect of eligible R&D activities (for the first $100 million of eligible expenditure):

a 43.5% refundable offset for eligible companies with aggregated annual turnover less than $20m; and

a 38.5% non-refundable tax offset for all other eligible companies.

Note that the Treasury Laws Amendment (Research and Development Tax Incentive) Bill 2019, before Parliament at the time the Federal Budget was released, proposed various amendments to the R&D Tax Incentive to take effect from the 2019-20 income year. The Government is now delaying (by two years) and enhancing the proposed changes.

Companies under $20m turnover

For companies with an aggregated annual turnover less than $20 million:

- The refundable R&D tax offset is being set at 18.5 percentage points above the claimant’s company tax rate (an increase from 13.5 percentage points above the claimant’s company tax rate as previously announced)

- The previously announced annual $4 million cap on cash refunds for R&D claimants will not proceed.

Companies over $20m turnover

For companies with aggregated annual turnover of $20 million or more, the previously announced R&D intensity premium, originally intended to apply across three tiers, will now apply across two tiers.

Note the intensity premium will tie the rates of the non-refundable R&D tax offset to the incremental intensity of R&D expenditure as a proportion of total expenditure for the year. The marginal R&D premium will be the company’s tax rate plus:

- 8.5 percentage points above the claimant’s company tax rate for R&D expenditure between 0 per cent and 2 per cent R&D intensity for larger companies

- 16.5 percentage points above the claimant’s company tax rate for R&D expenditure above 2 per cent R&D intensity for larger companies (the previously announced intensity premiums varied from 4.5 to 12.5 percentage points).

The R&D expenditure threshold – the maximum amount of R&D expenditure eligible for concessional R&D

tax offsets – will be increased as intended from $100 million to $150 million per annum.

Access to tax concessions extended to businesses up to $50m

Date of effect: Three phases: 1 July 2020, 1 April 2021, 1 July 2021

Announced pre Budget, a range of generous tax concessions normally only available to small and medium businesses, will be available to businesses with an aggregated turnover of up to $50 million.

The expanded concessions will be rolled out in three phases:

From 1

|

Immediate deduction for certain start-up expenses

Eligible new businesses can immediately deduct a range of professional expenses required to start up a business – such as professional, legal and accounting advice as well as amounts paid to Government agencies to set up the business entity. Immediate deduction for prepaid expenditure Eligible businesses can choose to claim an immediate deduction for prepaid expenses where the payment is for a period of service which is 12 months or less and ends in the next income year. |

From 1 April 2021

|

FBT cark parking exemption

Eligible employers will be exempt from FBT on certain car parking benefits provided to employees. FBT exemption on portable electronic devices Eligible employers will be able to provide more than one portable electronic device that is mainly for work use to an employee in a single FBT year and apply an FBT exemption (e.g., phones and laptops). |

From 1 July 2021 |

Simplified trading stock

Eligible businesses can choose not to conduct a stocktake if there is a difference of less than $5,000 between the opening value of trading stock and a reasonable estimate of the closing value of trading stock at the end of the income year. PAYG instalments based on GDP adjustment amount Eligible businesses can pay an ATO calculated PAYG instalment amount based on the last reported income (i.e., as reported in the most recent tax return) adjusted by a GDP adjustment factor. This removes the need to calculate the PAYG instalment each period based on a percentage of instalment income. Settle excise duty and excise-equivalent customs duty monthly On eligible goods, this concession enables eligible businesses to apply to defer settlement of their excise duty and excise equivalent customs duty from a weekly to a monthly reporting cycle. Two-year amendment period Eligible businesses will have a two-year amendment period apply to income tax assessments, excluding entities that have significant international tax dealings or particularly complex affairs. Simplified accounting methods The Commissioner of Taxation’s power to create a simplified accounting method determination for GST purposes will be expanded to apply to eligible businesses below the $50 million aggregated annual turnover threshold. |

The eligibility turnover thresholds for other small business tax concessions will remain at their current levels.

“Businesses with turnover under $5 billion can immediately deduct the full cost of eligible capital assets — an incentive designed to boost cash flow and support investment.”

FBT exemption for retraining and reskilling workers

Date of effect: 2 October 2020

Announced pre Budget, the Government will provide a Fringe Benefits Tax (FBT) exemption for employer-provided retraining and reskilling, for employees who are redeployed to a different role in the business.

Currently, if an employer provides a benefit to an employee that is not directly related to their current job, FBT applies. This measure enables employers to help employees reskill for a new role or another role with a different employer, without incurring FBT.

The exemption does not apply to retraining acquired through salary packaging or training provided through Commonwealth supported places at universities. The exemption also does not extend to repayments towards Commonwealth student loans.

The Government will also consult on potential changes to the law to allow a worker to deduct expenses they personally incur to undertake training directed at future employment and skills (current rules that limit deductions to training related to current employment, may act as a disincentive for workers to retrain and reskill).

Corporate residency test changes

Date of effect: First income year after the date of Royal Assent

Taxpayers have the option to apply the new law from 15 March 2017

The corporate residency tests will be clarified so that a company that is incorporated offshore will be treated as an Australian tax resident if it has a ‘significant economic connection to Australia’. This test will be satisfied if both:

- the company’s core commercial activities are undertaken in Australia, and

- its central management and control is in Australia.

Note that under current law, where a company is incorporated offshore, it is an Australian resident if both of the following apply:

- the company carries on business in Australia; and

- either:

-

- its central management and control is in Australia; or

- its voting power is controlled by Australian resident shareholders.

-

The announced change follows the High Court’s 2016 decision in Bywater Investments Ltd v Federal Commissioner of Taxation that departed from the long-held position on the definition of a corporate resident. Following this decision, the ATO issued TR 2018/5 effective from 15 March 2017 expressing its view that if a company has its central management and control in Australia, and it carries on business, it will carry on business in Australia for the purposes of the ‘central management and control’ test. In line with this view, a company will be an Australian resident for tax purposes notwithstanding the fact that no trading or investment operations of the business take place here. This was not the ATOs previous view set out in the now withdrawn TR 2004/15.

The Government’s announcement follows the Board of Taxation’s subsequent recommendation that amendments bring the treatment of foreign incorporated companies back to the position pre the 2016 court decision.

Managed investment trust withholding rate standardised across international information sharing agreements

Date of effect: 1 July 2021

The list of jurisdictions that have an effective information sharing agreement with Australia will be updated such that residents of those listed jurisdictions are eligible to access the reduced Managed Investment Trust (MIT) withholding tax rate of 15% on certain distributions, instead of the default rate of 30%.

The measure will add the Dominican Republic, Ecuador, El Salvador, Hong Kong, Jamaica, Kuwait, Morocco, North Macedonia and Serbia, and remove Kenya from the existing 122 jurisdictions on the list. These new jurisdictions have entered into information sharing agreements since the previous update in 2019.

100,000 new apprenticeships

Date of effect: 5 October 2020

Announced pre Budget, from 5 October 2020 a business (or Group Training Organisation) that takes on a new Australian apprentice will be eligible for a 50% wage subsidy, regardless of geographic location, occupation, industry or business size.

The scheme will be available until the 100,000 cap has been reached.

Under the subsidy, employers will be eligible for up to 50% of the wages of a new or recommencing apprentice or trainee for the period up to 30 September 2021. The maximum subsidy is $7,000 per quarter.

The subsidy is paid in arrears and is available for wages paid from 5 October 2020 to 30 September 2021.

Eligible businesses are those that:

- Engage an Australian Apprentice between 5 October 2020 and 30 September 2021, and

- The Australian Apprentice or trainee is undertaking a Certificate II or higher qualification, and has a training contract that is formally approved by the state training authority.

Specific regional COVID-19 funding measures

The Government has committed close to $552 million over four years from 2020-21 to assist regional Australia recover from the impacts of COVID-19 and recent natural disasters including:

- $207.7 million over five years from 2020-21 for round 5 of the Building Better Regions Fund

- $100 million over two years from 2020-21 to facilitate Regional Recovery Partnerships with states, territories and local governments in

- 10 priority investment regions

- $51 million over two years from 2020-21 to assist regions heavily reliant on international tourism

- $50.3 million over four years from 2020-21 to support the Rural Health Multidisciplinary Training program

- $41 million over three years from 2020-21 to support R&D activities in regional areas

- $30.3 million over two years from 2020-21 to extend Round One of the Regional Connectivity Program to improve access to digital technologies

If you have any questions about how any of these announcements affect you, please contact our team today.

About the author

Cayle Petritsch - Director & Wealth Advisor

Cayle Petritsch, Director and Wealth Advisor, works with our existing clients who have recognised the importance of business owners making strategic financial choices not only for their company, but for their personal finances too.

Cayle saw a great opportunity to expand North Advisory’s services into SMSF/superannuation, personal wealth management, asset protection services and other crucial personal finance facets that business owners need to consider.

His approach to wealth management allows you to receive highly personalised wealth advice. Working closely with Marius, Cayle understands the unique needs of every client, from their lifestyle and business goals to their retirement plans.

Key Takeaways

Economic Recovery Was the Priority

The Budget was framed around rebuilding the Australian economy and restoring confidence following the initial impact of COVID-19.

Businesses Were Encouraged to Invest

Measures like temporary full expensing aimed to drive business investment and improve cash flow.

Tax Relief Was Accelerated

Bringing forward personal tax cuts put more money into the hands of Australians sooner to support spending.

Driven by our values

Effortless and Seamless

On-Boarding Process

Intuitive and Knowledgeable

Direct Expert

Access

Useful and Articulate

Financial

Reporting

Forward

Thinking

Compliance Solutions

Streamlined

Tech

Integrated and Automated

Frequently Asked Questions

What was the main focus of the 2020 Federal Budget?

The 2020 Federal Budget focused heavily on economic recovery following COVID-19, with measures designed to support businesses, protect jobs and stimulate growth.

How did the Budget support businesses?

Support included incentives such as full expensing for eligible asset purchases, loss carry-back provisions, and extensions or refinements of existing COVID-related assistance.

Were there personal tax changes in the 2020 Budget?

Yes. The Budget brought forward elements of the personal income tax cuts, providing immediate relief to low- and middle-income earners.

What was announced in relation to JobKeeper?

The Budget confirmed the extension of JobKeeper payments, with stepped-down rates over time, to continue supporting eligible employers and employees during the recovery phase.

Did the Budget increase government spending and debt?

Yes. The 2020 Budget involved significant government spending and higher debt levels as part of a deliberate strategy to stimulate the economy and support employment.

What were the biggest takeaways from the 2020 Federal Budget for individuals and businesses?

North Advisory explains the 2020 Federal Budget focused heavily on economic recovery, with measures designed to support businesses, encourage hiring, and stimulate spending. Key themes included tax relief and incentives for business investment, along with targeted support aimed at keeping Australians employed and helping businesses rebuild confidence after the disruption of COVID-19.

North Advisory’s Reviews  On

On

Flo Mitchell

4 weeks ago

Changed to this company in 2019 from former accountant and love their approach of organizing everything for me face to face with Xero set up plus being able to call as much as I need for set annual fee. They also picked up on something that was not done correctly by my former accountant and saved me $4k for this.

Timothy Cummins

A month ago

They the truly the best, Martin and Judy are so experienced, knowledgeable & professonal, also quite like speaking with Rose : ) all people are so lovely!

Michael Iera

2 months ago

Positive, Responsiveness, Quality, Professionalism, Value

Michael Iera

2 months ago

Excellent company in regards to service and professionalism. Very experienced in dealing with complex matters. Highly recommended.

Reach out we are here to help

Recognising the uniqueness of each business, we specialise in customised accounting services crafted to meet your specific needs and drive business growth.

Don’t hesitate to contact us if you’re ready to streamline your financial management with tailored solutions. Your business’s success is our primary focus. Fill in the contact form or call us to book an initial 30-minute chat.

Suite 6, 11 Oaks Avenue

Dee Why, Northern Beaches

NSW 2099

Australia